6.4 Present Value of an Annuity and Installment Payment

Why do we care about the present value of an annuity? This idea shows up any time a stream of future payments is compared to money in hand today. It helps banks set mortgage payments and car loan payments, helps families plan retirement income, and helps lottery winners compare a lump-sum payout with an annuity payout over time. The core question is always the same: how much is a future stream of payments worth right now?

- Find the present value of an annuity.

- Find the amount of an installment payment on a loan.

In Section 6.3, we moved forward in time to find the future value of an annuity. In this section, we reverse that process. We start with payments that will happen later and ask what single amount today would be financially equivalent.

Present Value of an Annuity

In Section 6.2, we learned how to find the future value of a lump sum, and in Section 6.3, we learned how to find the future value of an annuity. Now we use those ideas to study loan amortization and the present value of an annuity.

The present value of an annuity is the amount of money we would need now in order to make the payments in the annuity later. In other words, it is the value today of a future stream of payments.

We will first break the idea down step by step so the meaning is clear. After that, we will use a more efficient algebraic method based on ideas we already developed in Sections 6.2 and 6.3.

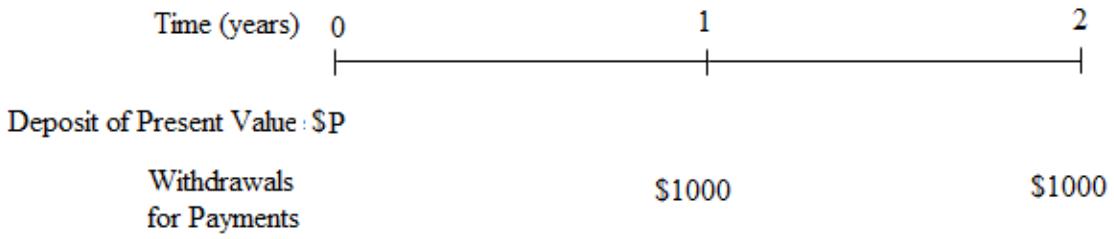

Suppose Carlos owns a small business and employs an assistant manager to help run it. Assume it is January 1 right now. Carlos plans to pay his assistant manager a \$1000 bonus at the end of this year and another \$1000 bonus at the end of the following year.

Carlos' business had a good year, so he wants to put the money for those future bonuses into a savings account now. The money he deposits now will earn interest at the rate of \(4\%\) per year, compounded annually.

How much money should Carlos put into the savings account now so that he will be able to withdraw \$1000 one year from now and another \$1000 two years from now?

At first this may sound like a sinking fund, but it is different. In a sinking fund, we make periodic deposits in order to build up to a specified future value. Here, Carlos is doing the opposite: he wants to deposit one lump sum now and later withdraw a series of payments.

That means the amount deposited now is the principal \(P\), and the withdrawals form an annuity with payments of \$1000 at the end of each year.

We want to determine the amount needed in the account now so that those future withdrawals are possible.

We use the compound interest formula from Section 6.2 with \(r = 0.04\) and \(n = 1\) for annual compounding to determine the present value of each \$1000 payment.

Consider the first payment of \$1000 at the end of year 1. Let \(P_1\) be its present value.

$$ 1000 = P_1(1.04)^1 \qquad \text{so} \qquad P_1 = \$961.54 $$Now consider the second payment of \$1000 at the end of year 2. Let \(P_2\) be its present value.

$$ 1000 = P_2(1.04)^2 \qquad \text{so} \qquad P_2 = \$924.56 $$To make the \$1000 payments at the specified times in the future, Carlos must deposit the sum of those present values now:

$$ P = P_1 + P_2 = \$961.54 + \$924.56 = \$1886.10 $$The farther away a payment is, the smaller its present value is. That is why the second \$1000 payment is worth less today than the first one. Money has time to earn interest, so future dollars are discounted when we bring them back to the present.

The step-by-step calculation above is useful because it shows what present value really means. But it is not efficient when there are many annuity payments. For a long annuity, we want a faster method.

If a payment of \(m\) dollars is made in an account \(n\) times a year at interest rate \(r\) for \(t\) years, then the present value \(P\) satisfies

$$ P\left(1 + \frac{r}{n}\right)^{nt} = \frac{m\left[\left(1 + \frac{r}{n}\right)^{nt} - 1\right]}{r/n} \tag{Formula 6.4.1} $$This formula assumes that the payment period and the compounding period are the same.

Source: Applied Finite Math

Suppose you will receive \$500 at the end of each year for the next 3 years, and money can earn \(5\%\) compounded annually. What is the present value of this annuity?

Try It Now 6.4.1 Solution

Use Formula 6.4.1 with \(m = 500\), \(r = 0.05\), \(n = 1\), and \(t = 3\).

$$ P(1.05)^3 = \frac{500\left[(1.05)^3 - 1\right]}{0.05} $$Since \((1.05)^3 = 1.157625\), we get

$$ P(1.157625) = 500(3.1525) = 1576.25 $$ $$ P = \frac{1576.25}{1.157625} \approx \$1361.62 $$Source: Applied Finite Math

Suppose you have won a lottery that pays \$1000 per month for the next 20 years. But you prefer to have the entire amount now. If the interest rate is \(8\%\), how much should you accept?

Example 6.4.1 Solution

This is a classic present value problem, and the reasoning we use here will also help with the loan problems that follow.

Imagine that two people, Mr. Cash and Mr. Credit, have won the same lottery of \$1000 per month for the next 20 years. Mr. Credit is happy receiving the monthly payments, but Mr. Cash wants a lump sum today.

Our goal is to find how much money Mr. Cash should get.

If Mr. Cash accepts \(P\) dollars now, then that lump sum invested at \(8\%\) compounded monthly for 20 years should grow to the same future value as the annuity received by Mr. Credit.

So we compare the future values of:

- the lump sum accepted now, and

- the annuity of monthly payments.

Since Mr. Cash receives a lump sum of \(P\) dollars, its future value is given by the lump sum formula from Section 6.2:

$$ A = P\left(1 + \frac{0.08}{12}\right)^{240} $$Since Mr. Credit receives an annuity of \$1000 per month, its future value is given by the annuity formula from Section 6.3:

$$ A = \frac{1000\left[\left(1 + \frac{0.08}{12}\right)^{240} - 1\right]}{0.08/12} $$Mr. Cash will agree to the lump sum only if these two future values are equal. So we set them equal and solve for \(P\).

$$ P\left(1 + \frac{0.08}{12}\right)^{240} = \frac{1000\left[\left(1 + \frac{0.08}{12}\right)^{240} - 1\right]}{0.08/12} $$Using calculator values,

$$ P(4.9268) = 1000(589.02041) $$ $$ P(4.9268) = 589020.41 $$ $$ P = \$119,554.36 $$Therefore, the present value of an ordinary annuity of \$1000 each month for 20 years at \(8\%\) is \$119,554.36.

If Mr. Cash takes his lump sum of \(P = \$119,554.36\) and invests it at \(8\%\) compounded monthly, he will have an accumulated value of

$$ A = \$589,020.41 $$in 20 years, which matches the future value of the annuity.

This kind of reasoning is exactly what is used when a lottery winner must choose between a lump sum now and annuity payments over time. The same idea also appears in retirement planning, where you may ask: what single amount today is equivalent to a stream of monthly withdrawals in the future?

Installment Payment on a Loan

If a person or business needs to pay for something now—such as a car, a home, college tuition, or business equipment—but does not currently have the money, they can borrow it as a loan.

They receive the loan amount, called the principal or present value, now and then repay that amount over time with regular payments plus interest.

When the loan is paid off gradually through regular payments, we say the loan is amortized.

This is the mathematics behind monthly car payments, mortgage payments, tuition payment plans, and equipment financing for businesses. Lenders need to know the correct payment amount so that the loan is fully repaid by the end of the term.

Principal is the amount borrowed now.

Installment payment is the regular payment made each period.

Term of the loan is the total length of time over which the loan is repaid.

Amortization means repaying a loan through a sequence of scheduled payments.

Source: Applied Finite Math

Find the monthly payment for a car costing \$15,000 if the loan is amortized over five years at an interest rate of \(9\%\).

Example 6.4.2 Solution

Again, imagine the following scenario.

Two people, Mr. Cash and Mr. Credit, go to buy the same car that costs \$15,000. Mr. Cash pays cash and drives away, but Mr. Credit wants to make monthly payments for five years.

Our job is to determine the amount of the monthly payment.

If Mr. Credit pays \(m\) dollars per month, then those monthly payments, accumulated at \(9\%\) for 5 years, should yield the same future value as a \$15,000 lump sum accumulated for 5 years.

Again, we compare the future values of the lump sum and the annuity and require them to be equal.

Since Mr. Cash pays a lump sum of \$15,000, its future value is given by the lump sum formula:

$$ 15000\left(1 + \frac{0.09}{12}\right)^{60} $$Mr. Credit makes an annuity of \(m\) dollars per month, so its future value is given by the annuity formula:

$$ \frac{m\left[\left(1 + \frac{0.09}{12}\right)^{60} - 1\right]}{0.09/12} $$Set the two future amounts equal and solve for the unknown:

$$ 15000\left(1 + \frac{0.09}{12}\right)^{60} = \frac{m\left[\left(1 + \frac{0.09}{12}\right)^{60} - 1\right]}{0.09/12} $$Using calculator values,

$$ 15000(1.5657) = m(75.4241) $$ $$ m = \$311.38 $$Therefore, the monthly payment needed to repay the loan is \$311.38 for five years.

When Formula 6.4.1 is used for a loan, \(P\) is the loan amount and \(m\) is the periodic payment. Solving for \(m\) gives

$$ m = \frac{P\left(1 + \frac{r}{n}\right)^{nt}(r/n)}{\left(1 + \frac{r}{n}\right)^{nt} - 1} $$This formula is valid when the payment period and compounding period are the same.

Source: Applied Finite Math

Find the monthly payment on a loan of \$12,000 amortized over 4 years at an interest rate of \(6\%\) compounded monthly.

Try It Now 6.4.2 Solution

Use the installment payment formula with \(P = 12000\), \(r = 0.06\), \(n = 12\), and \(t = 4\).

$$ m = \frac{12000\left(1 + \frac{0.06}{12}\right)^{48}(0.06/12)}{\left(1 + \frac{0.06}{12}\right)^{48} - 1} $$Since \(\left(1 + \frac{0.06}{12}\right)^{48} \approx 1.2705\),

$$ m \approx \frac{12000(1.2705)(0.005)}{1.2705 - 1} \approx \$281.90 $$Section 6.4 Summary

We summarize the method used in Examples 6.1 and 6.2 below.

If a payment of \(m\) dollars is made in an account \(n\) times a year at interest rate \(r\), then the present value \(P\) of the annuity after \(t\) years is

$$ P\left(1 + \frac{r}{n}\right)^{nt} = \frac{m\left[\left(1 + \frac{r}{n}\right)^{nt} - 1\right]}{r/n} $$When used for a loan, \(P\) is the loan amount and \(m\) is the periodic payment needed to repay the loan over a term of \(t\) years with \(n\) payments per year.

- If the present value or loan amount is needed, solve for \(P\).

- If the periodic payment is needed, solve for \(m\).

- The formula assumes that the payment period is the same as the compounding period.

Finally, note that many finite mathematics and finance books develop the present value formula differently. Instead of beginning with

$$ P\left(1 + \frac{r}{n}\right)^{nt} = \frac{m\left[\left(1 + \frac{r}{n}\right)^{nt} - 1\right]}{r/n} \tag{Formula 6.4.1} $$and then solving for \(P\) after substituting numerical values, many textbooks first solve the formula symbolically for \(P\) to create a separate present value formula.

Alternate Method to Find Present Value of an Annuity

Starting with Formula 6.4.1,

$$ P\left(1 + \frac{r}{n}\right)^{nt} = \frac{m\left[\left(1 + \frac{r}{n}\right)^{nt} - 1\right]}{r/n} $$divide both sides by \(\left(1 + \frac{r}{n}\right)^{nt}\) to isolate \(P\) and simplify:

$$ P = \frac{m\left[\left(1 + \frac{r}{n}\right)^{nt} - 1\right]}{r/n} \cdot \frac{1}{\left(1 + \frac{r}{n}\right)^{nt}} $$ $$ P = \frac{m\left[1 - \left(1 + \frac{r}{n}\right)^{-nt}\right]}{r/n} \tag{Formula 6.4.2} $$Formula 6.4.2 is mathematically correct, but some students find Formula 6.4.1 easier to learn because it avoids introducing a second formula right away. The tradeoff is that Formula 6.4.2 is ready to use directly for present value, while Formula 6.4.1 requires you to solve algebraically for \(P\) when needed.

The authors of this book believe it is easier to use Formula 6.4.1 and solve for \(P\) or \(m\) as needed. In that approach, there are fewer formulas to memorize, and many students find it easier to learn.

However, some people prefer Formula 6.4.2, and it is mathematically correct to use that method. If you choose Formula 6.4.2, be careful with the negative exponent. Also notice that if you need the periodic payment, you still have to do algebra to solve for \(m\).

It is a good idea to check with your instructor to see whether he or she prefers one method over the other.

Source: Applied Finite Math

Use Formula 6.4.2 to find the present value of an annuity that pays \$800 every year for 6 years at \(7\%\) compounded annually.

Try It Now 6.4.3 Solution

Use \(m = 800\), \(r = 0.07\), \(n = 1\), and \(t = 6\).

$$ P = \frac{800\left[1 - (1.07)^{-6}\right]}{0.07} $$Since \((1.07)^{-6} \approx 0.6663\),

$$ P \approx \frac{800(1 - 0.6663)}{0.07} = \frac{800(0.3337)}{0.07} \approx \$3813.71 $$Section 6.4 Problem Set: Present Value of an Annuity and Installment Payment

Source: Applied Finite Math

For the following problems, show all work.

Problem 1. Shawn has won a lottery paying him \$10,000 per month for the next 20 years. He'd rather have the whole amount in one lump sum today. If the current interest rate is 8.2%, how much money can he hope to get?

Problem 2. Sonya bought a car for \$15,000. Find the monthly payment if the loan is to be amortized over 5 years at a rate of 10.1%.

Problem 3. You determine that you can afford \$250 per month for a car. What is the maximum amount you can afford to pay for a car if the interest rate is 9% and you want to repay the loan in 5 years?

Problem 4. Compute the monthly payment for a house loan of \$200,000 to be financed over 30 years at an interest rate of 10%.

Problem 5. If the \$200,000 loan in the previous problem is financed over 15 years rather than 30 years at 10%, what will the monthly payment be?

Problem 6. Friendly Auto offers Jennifer a car for \$2000 down and \$300 per month for 5 years. Jason wants to buy the same car but wants to pay cash. How much must Jason pay if the interest rate is 9.4%?

For the following problems, show all work.

Problem 7. The Gomez family bought a house for \$450,000. They paid 20% down and amortized the rest at 5.2% over a 30-year period. Find their monthly payment.

Problem 8. Mr. and Mrs. Wong purchased their new house for \$350,000. They made a down payment of 15%, and amortized the rest over 30 years. If the interest rate is 5.8%, find their monthly payment.

Problem 9. A firm needs a piece of machinery that has a useful life of 5 years. It has an option of leasing it for \$10,000 a year, or buying it for \$40,000 cash. If the interest rate is 10%, which choice is better?

Problem 10. Jackie wants to buy a \$19,000 car, but she can afford to pay only \$300 per month for 5 years. If the interest rate is 6%, how much does she need to put down?

Problem 11. Vijay's tuition at college for the next year is \$32,000. His parents have decided to pay the tuition by making nine monthly payments. If the interest rate is 6%, what is the monthly payment?

Problem 12. Glen borrowed \$10,000 for his college education at 8% compounded quarterly. Three years later, after graduating and finding a job, he decided to start paying off his loan. If the loan is amortized over five years at 9%, find his monthly payment for the next five years.